Pre-Open Data

Key Data for the Week

Key economic data released this week:

- Wednesday – CHINA – Consumer Price Index fell 0.5% in the 12 months to November. It was the first time since 2009 that the annual rate of consumer price inflation had turned negative.

- Thursday – EUR – ECB Interest Rate Decision

- Thursday – UK – Gross Domestic Product

- Thursday – US – Consumer Price Index

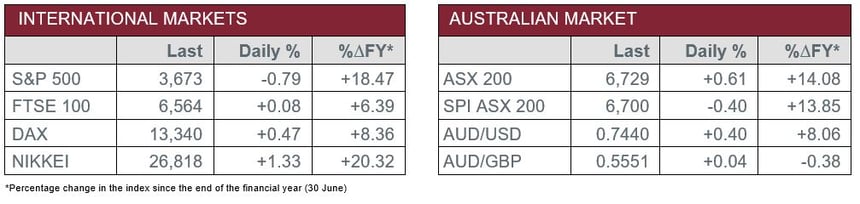

Australian Market

The Australian sharemarket rose 0.6% yesterday, to close higher for the seventh-straight session. The Health Care sector was the strongest performer, led higher by CSL, up 2.2%. Healius climbed 7.4% after the company announced it will complete a $200 million on market share buy-back over the next twelve months and a trading update which noted strong and sustained revenue growth in its pathology and imaging divisions.

Commonwealth Bank rose 1.7% after the company revealed it will receive more than first expected from the sale of its stake in a Chinese life insurance provider, BoCommLife. The bank said it will receive $886 million from the sale. Among the other big banks, NAB rose 0.6%, while ANZ and Westpac fell 0.4% and 0.3% respectively.

Mining heavyweights continued to climb, along with the price of iron ore; Fortescue Metals rose 1.6% to hit a record high, while BHP and Rio Tinto gained 1.1% and 0.4% respectively.

The REITs and Energy sectors were the only two sectors to close lower.

The Australian futures market points to a 0.40% fall today.

Overseas Markets

European sharemarkets closed higher on Wednesday, while closing off best levels as investors awaited the outcome of Brexit trade talks between UK Prime Minister Boris Johnson and European Commission President Ursula von der Leyen held in Brussels overnight. HelloFresh rose 4.7% after the company provided a trading update and increased FY20 guidance of revenue growth to 107-112%.

US sharemarkets were weaker overnight, dragged lower by Information Technology and Communication Services stocks. Alphabet, Amazon, Apple, Facebook and Microsoft all fell between 1.9% and 2.3%, while Telecommunications company AT&T outperformed to rise 2.1%. Renewable energy companies SolarEdge Technology and Enphase Energy slipped 4.6% and 5.6% respectively.

By the close of trade, the Dow Jones slipped 0.4%, S&P 500 lost 0.8% and the NASDAQ fell 1.9%.

CNIS Perspective

No longer is the world of gaming dominated by teenage boys playing in their parents' basement. Today ‘gamers’ reach a far wider spectrum including millennials, as well as the expanding ranks of female gamers and diverse users in countries around the world.

Already dominating global entertainment, the once niche segment of games has grown into a US$150 billion industry. The video game business is now larger than both the movie and music industries combined.

One way to put into perspective the size of the industry, is referring to 2018 data that compared Netflix and game viewing on YouTube. Netflix streamed 51 billion hours of watch-time on their platform in 2018, while over 50 billion hours of gaming was watched in the same year.

Another surprisingly large number is the sale of virtual goods, which now generates revenue of about US$130 billion around the world. These purchases are non-physical objects, used in online communities and online games.

Often dismissed as a niche area, the expectation is that this industry will double over the next five years, with a projected annual compound growth rate of more than 20%.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.