Pre-Open Data

Key Data for the Week

Key economic data released this week:

- Wednesday – US – Housing Starts continued to recover, with figures ahead of expectations. During October a total of 1,530,000 homes and apartments were constructed.

- Thursday – AUS – Unemployment Rate

Australian Market

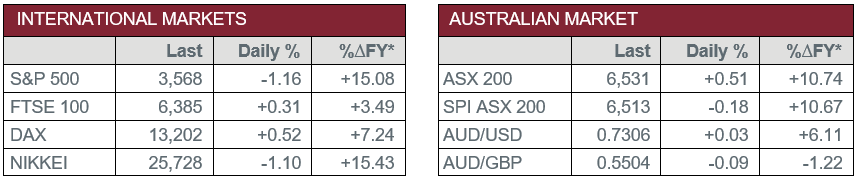

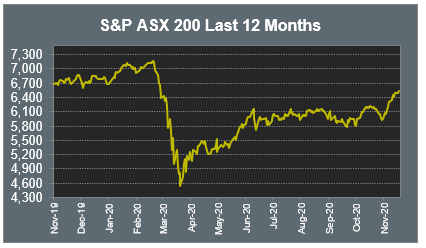

The Australian sharemarket rose 0.5% in a mixed session of trade. The Financials sector led the gains as the big four banks all rose between 1.3% and 2.9%, led by Commonwealth Bank. Wealth managers Australian Ethical Investment and Magellan Financial Group added 1.9% and 1.2% respectively, while investment bank Macquarie Group slipped 0.4%.

Consumer stocks also rallied; Coles and Wesfarmers gained 1.7% and 1.4% respectively, while Woolworths rose 0.6%. Crown Resorts fell 0.6%, after the company was briefly in a trading halt following NSW Independent Liquor and Gaming Authority’s decision to withhold approval of the opening of its Barangaroo Casino in December.

Telstra slipped 1.3% to weigh on the Telecommunications sector, while mining heavyweights BHP, Fortescue Metals and Rio Tinto all fell between 0.5% and 0.7% to drag the Materials sector lower.

The Energy sector weakened from recent strength; Oil Search and Santos fell 2.6% and 1.8% respectively, however, Woodside Petroleum bucked the trend to gain 0.5%.

Travel stocks also fell from recent highs; Qantas lost 1.4%, Sydney Airport was down 0.9% and Auckland International Airport fell 0.7%. Toll road operator Transurban Group bucked the trend to add 1.6%.

The Australian futures market points to a 0.18% fall today.

Overseas Markets

European sharemarkets closed higher on Wednesday, as investor sentiment was lifted with more positive updates on the COVID-19 vaccine, however, this was partially offset by the ongoing number of cases. By the close of trade, the broad based STOXX Europe 600 rose 0.4%.

US sharemarkets weakened overnight, with the Energy, Utilities and Health Care sectors the weakest performers. Pfizer and BioNTech rose 0.8% and 4.0% respectively, after the companies announced a 95% success rate of their vaccine trial.

By the close of trade, the Dow Jones and S&P 500 both fell 1.2%, while the NASDAQ lost 0.8%.

CNIS Perspective

Following the US election, the world looks to be united in the interests of sustainability once again.

President-elect Joe Biden has committed to re-entering the Paris Agreement on day one of his administration, with a series of initiatives planned to change the way US citizens interact with the environment in their daily lives.

In the area of transport, the administration has committed to building 500,000 new public electric vehicle charging stations by 2030 and announcing a plan, but not a date, to ban the sale of new petrol and diesel vehicles.

This is not just a theme of regulation in the US. Many European countries, including the UK, France and Denmark, have committed to banning the sale of fossil fuel cars by 2030. China has also committed, albeit without a date.

Australia has not yet entertained the conversation, though some advocates, such as the NRMA, believe that a date of 2025 is warranted.

In their 2020 report on the Electric Vehicle Outlook, Bloomberg estimates 29.2% of vehicles sold in 2030 across the US and Europe will be electric, up from 2.6% in 2019, and the electric charging infrastructure industry in those countries will be worth US$60bn in 2030 and US$192bn by 2040.

We wait to see how this secular change in transportation will affect the automotive and oil industries and how these established companies will adapt and survive the legislative disruption.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.