-1.png)

Weekly recap

What happened in markets

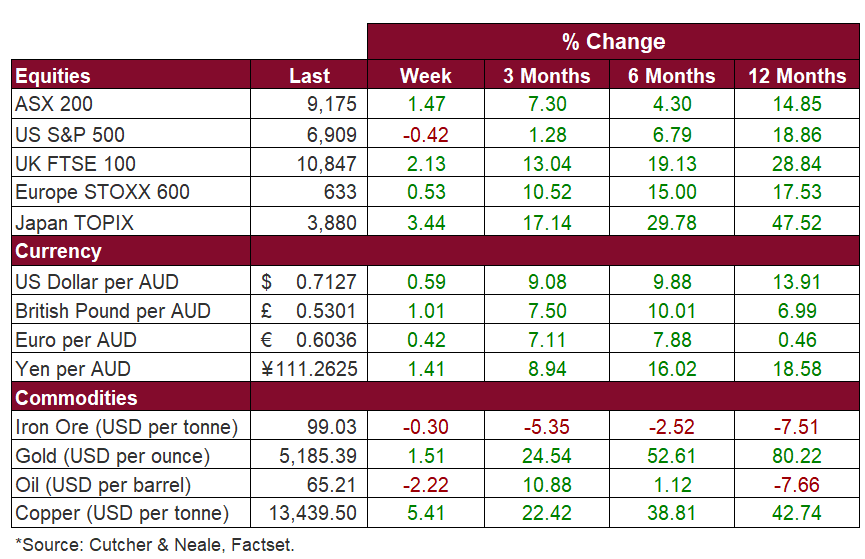

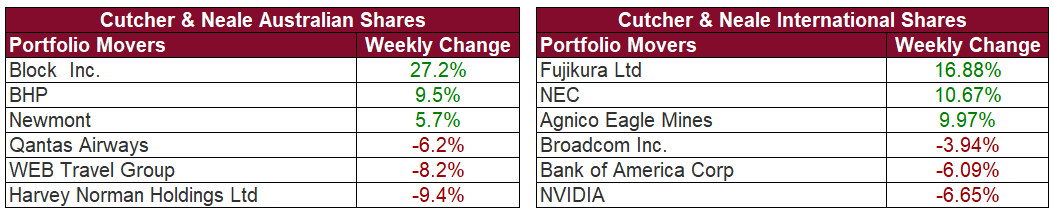

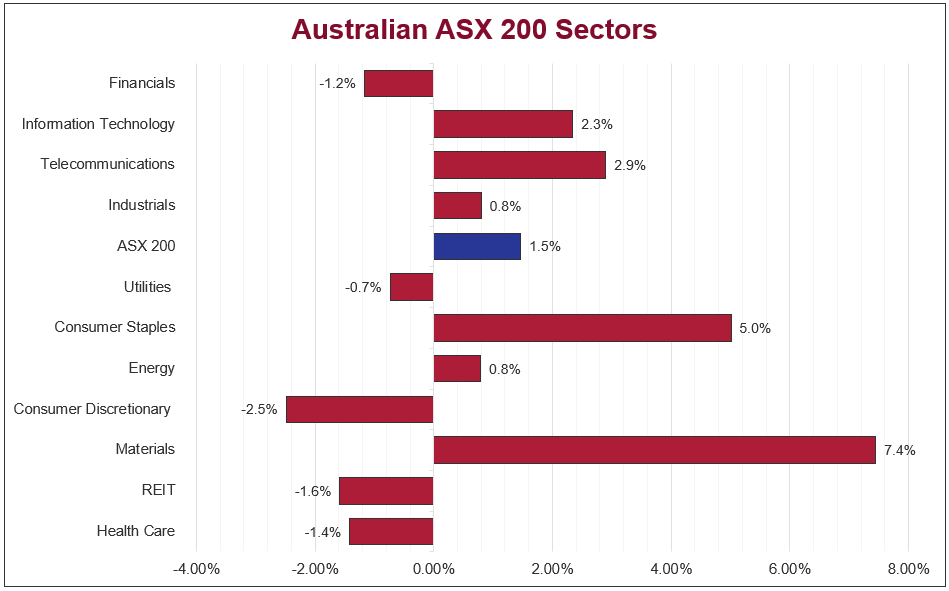

The Australian sharemarket rose 1.5% last week, recording its strongest February performance since 2019. Gains were led by the Telecommunications (2.9%), Information Technology (2.3%) and Materials (7.4%) sectors, while Consumer Staples (5.0%) also advanced. Health Care (-1.4%), REITs (-1.6%), Consumer Discretionary (-2.5%), Financials (-1.2%) and Utilities (-0.7%) lagged. Within the Cutcher & Neale Australian Shares Model, Block Inc. was the standout performer, surging 27.2% following its fourth-quarter and full-year results. Other contributors included BHP (+9.5%) and Newmont (+5.7%), while Qantas (-6.2%), WEB Travel Group (-8.2%) and Harvey Norman (-9.4%) detracted from returns.

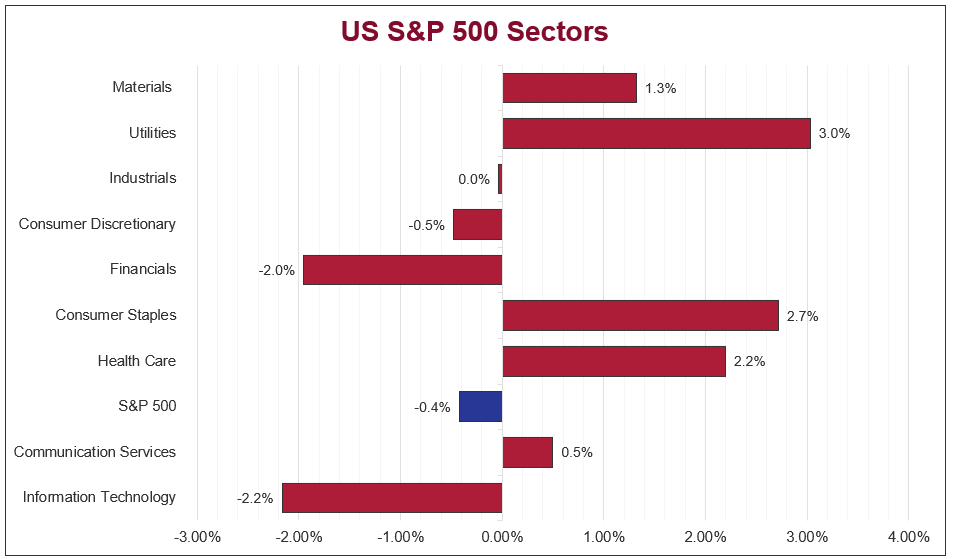

US sharemarkets finished lower last week, with the S&P 500 down -0.4% and the NASDAQ falling -0.9%, as concerns over AI disruption weighed on large-cap technology stocks. Information Technology (-2.2%) and Financials (-2.0%) sectors led losses, with NVIDIA (-6.7%) weighing on tech stocks, alongside broader semiconductor weakness and positioning-driven selling. The Consumer Discretionary (-0.5%) sector also softened amid mixed earnings results. In contrast, defensive and cyclical sectors outperformed, with Utilities (+3.0%), Consumer Staples (+2.7%), Health Care (+2.1%), Energy (+2.0%) and Materials (+1.3%) sectors supporting markets last week, benefitting from safe-haven flows, strong commodity prices, and better-than-expected corporate earnings.

European sharemarkets finished slightly higher last week, with the STOXX Europe 600 up 0.5%, as risk sentiment remained resilient despite geopolitical and policy uncertainties. Utilities (+4.6%) and Energy (+2.8%) sectors led gains, supported by strong corporate earnings, capital allocation plans, and firming oil prices amid US-Iran tensions. Basic Resources and Telecommunications sectors also outperformed, while Health Care, Construction & Materials, and Travel & Leisure sectors lagged. Investor focus was on US trade policy, after the Supreme Court struck down IEEPA tariffs, replaced by a lower 10% Section 122 levy.

Stock & sector movements

What caught our eye

Markets were rattled last week, triggered by artificial intelligence (AI) fears. Sentiment has been soft since Anthropic (US-based AI developer most notably backed by Amazon) introduced Claude Cowork, its latest experimental agentic AI model. Agentic meaning AI that can independently take actions and make decisions, rather than just responding to prompts. Meanwhile, Citrini Research’s memo, “The 2028 Global Intelligence Crisis”, gave us the ultimate “what if”. Citrini is known for big-picture, provocative research that often explores tail-risk scenarios others won’t touch.

What happened

A fictional macro memo from the future, Citrini’s story outlines a world set in 2028 where AI was too successful. Enhanced productivity leads to a collapse in white-collar employment, a consumer slowdown and eventual credit crisis. While the authors pose this as a scenario (a highly negative one) not a prediction, investors paid attention.

The 5 key points were:

-

AI-driven productivity boom turns into a demand collapse as workers lose their jobs.

-

A self-reinforcing intelligence displacement spiral. Companies cut staff to fund AI, enabling further layoffs.

-

Agentic commerce (where autonomous AI agents help optimise and execute purchasing decisions) destroys existing business models.

-

Corporate credit providers see higher defaults and become distressed.

-

Mortgage stress accelerates, raising the risk of a GFC-style event.

Bloomberg described an “AI scare trade” that sent shares in software, payments and delivery names sharply lower. IBM’s worst drop in decades was the headline grab, but it was broader than that, with DoorDash, American Express, Visa, Mastercard and various private credit-linked names also hit. Cybersecurity names were also weaker following Anthropic’s Claude Code Security announcement, including CrowdStrike, Palo Alto and Zscaler.

It all sounds bad and conceptually plausible. Scenario exercises can be useful. However, forecasting years ahead, particularly with disruptive technology, is fraught with danger and worst-case “what ifs” can be seductive.

What we tend to agree with…

-

There is risk of higher unemployment in the near-term (though reduced participation may obscure the numbers).

-

Corporate profits will be strong.

-

Existing company business models will be challenged. AI will create winners and losers.

-

AI will help ease inflation via improved productivity.

What we tend to disagree with…

-

We don’t buy into ‘software is dead’ or ‘cybersecurity is dead’ stories. There will be winners, losers and restructuring. AI providers will work with, not replace companies.

-

Real wages won’t collapse. Workers will use AI to be more productive. Expertise/specialisation will become more valuable. Nominal wages growth may slow, but so too will inflation.

-

The velocity of these forces is unlikely to be as extreme as suggested.

What this means for investors

The danger for investors is mistaking coherence for probability. Real economies don’t sit still. Policy, regulation, consumer behaviour, labour markets, company strategy and competitive dynamics adjust. The report’s own “no natural brake” feedback loop makes for gripping reading, but it arguably downplays the many ways society tries to install brakes once the pain gets real.

That said, dismissing such scenarios outright would be wrong. It’s times like this where keeping a level head and managing the risks is critical. The right way to think is “what’s the probability and what are the payoffs”. A scenario that sounds horrible but has a 5-10% probability is not a reason to upend your strategy. It calls for understanding the risks, positioning for opportunity and avoiding costly overreactions to short-term narratives.

The week ahead

Australian investors will be watching February’s inflation data on Monday and Q4 GDP on Wednesday for insights into economic growth and potential RBA policy moves. In the US, Q4 earnings season is winding down, with most results already priced in.

Market focus, however, remains on heightened Middle East tensions over the weekend, which have boosted safe-haven demand. Oil and copper prices continue to be sensitive to geopolitical risks and supply concerns, while broader risk sentiment may also be influenced by developments in trade and energy markets.

Wade is the head of the Investment Services division at Cutcher & Neale and has over 15 years of industry experience in accounting and investment advisory roles.

Wade guides his division on the belief that investment portfolios should be built on transparency and flexibility. His expertise focuses on direct portfolio exposure to both Australian and Global Investment markets.

-1.png?width=352&name=Investment%20SnapShot%20Header%20-%20July%202025%20(1)-1.png)