-1.png)

Weekly recap

What happened in markets

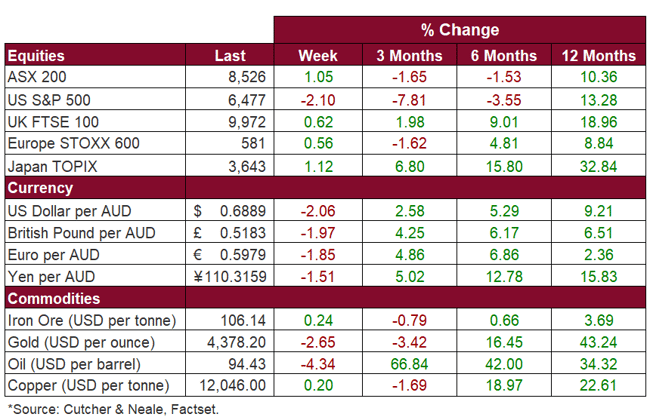

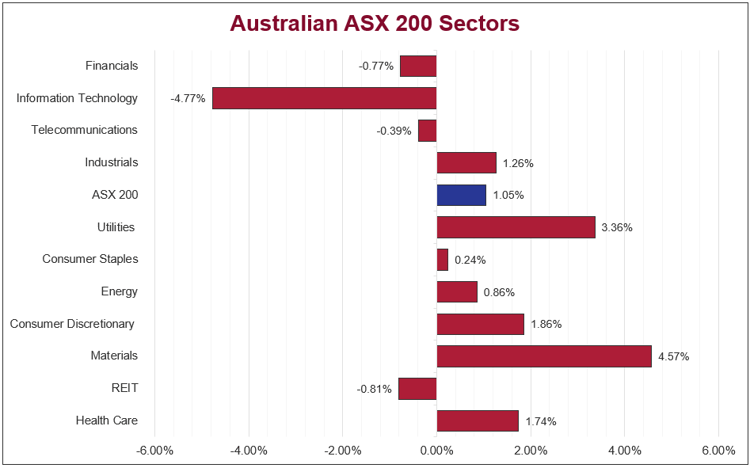

The Australian sharemarket rebounded last week, with the ASX 200 rising 1.1% after snapping a three-week decline. Volatility was driven by ongoing Iran-US tensions, with markets reacting sharply to mixed diplomacy headlines. The Materials sector (4.6%) led gains, supported by a metals rally on ceasefire optimism, while Industrials (1.3%) and Health Care (1.7%) also advanced. The Energy sector (0.9%) showed resilience, buoyed by crude movements and Middle East supply concerns, despite some coal and oil names retreating midweek. Information Technology (-4.8%) lagged to near three-year lows amid persistent AI disruption fears. Bond yields rose, keeping risk appetite cautious.

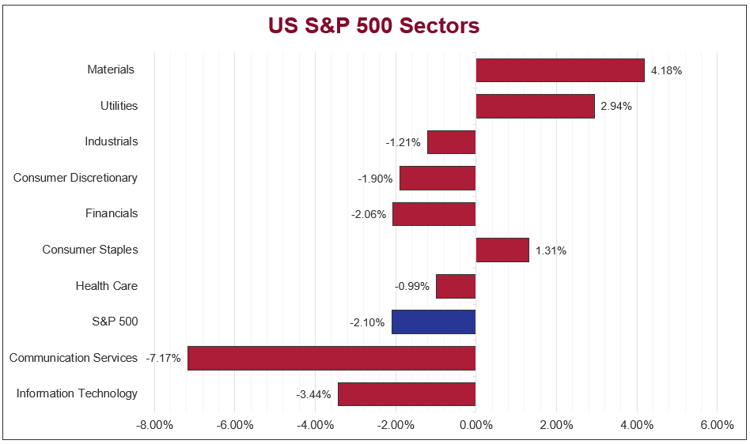

US sharemarkets were weaker last week, with the S&P 500 (-2.1%) and NASDAQ (-3.2%) declining, as geopolitical uncertainty and continued weakness in technology stocks weighed on sentiment. The Iran conflict remained a key focus, driving volatility amid shifting de-escalation headlines. The Information Technology sector (-3.4%) was a key drag, pressured by declines in big tech, semiconductors, and software, while the Communication Services sector (-7.2%) also saw notable weakness. In contrast, the Energy sector (6.2%) outperformed on higher oil prices, with the Materials sector (4.2%) also stronger on gains by commodity-linked names.

European sharemarkets were modestly higher last week, with the STOXX Europe 600 up 0.6%, supported by a rebound in cyclical and commodity-linked sectors amid ongoing Middle East tensions. The Basic Resources sector (3.4%) led gains, buoyed by stronger commodity prices, while Automobile & Parts (2.2%) and Energy (1.8%) also advanced on elevated energy prices and robust industrial activity. In contrast, the Technology sector (-1.6%) and Financial Services sector (-1.3%) lagged, pressured by cooling AI sentiment, semiconductor weakness, and private credit concerns. Volatility persisted as investors weighed energy risks and broader macro uncertainty.

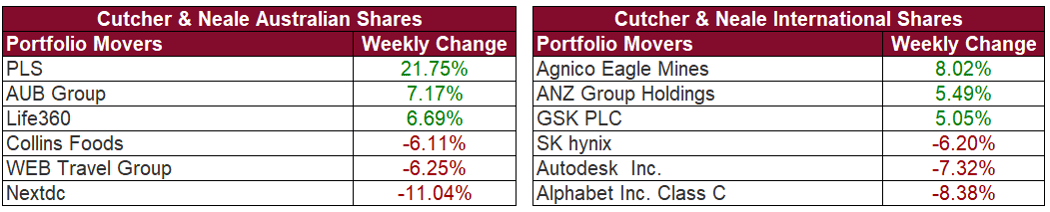

Stock & sector movements

What caught our eye

Markets have again reminded us that investor risk appetite can turn fast. There has been plenty to be fearful of, if investors choose to lean into the rhetoric. The main stories right now are:

-

The conflict in the Middle East,

-

The associated oil supply shock,

-

Artificial intelligence's (AI) potential disruption to the workforce and,

-

The lingering US debt situation (worsened by defense spending and higher interest rates)

The instinctive focus on available risk serves humans well, but it is rarely helpful for investors. Often the impact of risks is misjudged or exaggerated, or the series of events are so unknown you can’t do anything useful about them.

This is not to say the risks aren’t real. The conflict in the Middle East is dire and uncertain. The associated oil supply shock is being felt by everyone globally. A big reason is the Strait of Hormuz, one of the world’s most important shipping routes for energy. A large share of global oil and fertiliser supply normally moves through that passage, so any disruption there quickly affects energy and food prices beyond the region. When cargo cannot move as planned, supply does not reach refineries or farmers in the usual way, shipping schedules are thrown off and markets tighten fast. At the same time, countries become more focused on protecting their own supplies, which limits how markets can adjust. The result has been a sharp rise in oil and fertiliser prices. For households, that shows up at the petrol pump and grocery checkouts. For markets, it raises fresh concerns around inflation, growth and interest rates.

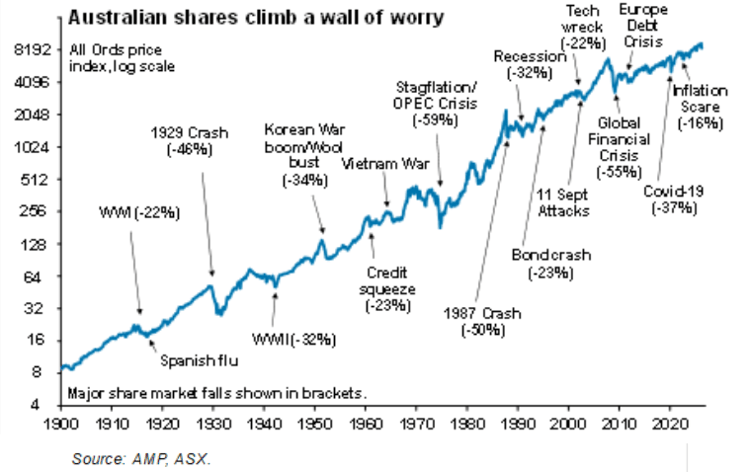

While the risks are real, that doesn’t necessarily mean immediate investment action is required. Markets always have had something to worry about. War, inflation, recessions, elections and policy mistakes are nothing new. Long-term investors have historically been rewarded for staying invested. That does not mean every setback is small. Some are not. But it does mean that selling into fear has usually been a poor strategy. The probability of timing it right is low and if you’re successful it’s likely to be more luck than skill.

Times like these are where discipline matters most. It’s also where having a financial adviser and investment manager often pays off.

There is a lot of noise in markets, particularly if you focus on headlines. Oil is one issue, AI is another. In both cases, the market has swung between excitement and fear. But the real investment outcomes are unlikely to be so simple. Not every business will be hurt in the same way and not every winner has been found. Importantly, not every risk justifies a major portfolio change. Particularly those that have already moved markets and are likely to prove temporary or extremely unpredictable. Incremental changes may indeed be necessary but should only be done with a level head and long-term mindset.

Periods like this can feel uncomfortable. But they also shape long-term returns. In our view, the investors who come through them best are usually the ones who filter out the noise, remain patient and keep looking ahead.

The week ahead

Locally, the key focus will be Tuesday’s RBA minutes from the March policy meeting, which may provide insight into the 25bp rate hike to 4.10%.

In the US, investors will watch February Retail Sales and ADP Employment (Wednesday).

Wade is the head of the Investment Services division at Cutcher & Neale and has over 15 years of industry experience in accounting and investment advisory roles.

Wade guides his division on the belief that investment portfolios should be built on transparency and flexibility. His expertise focuses on direct portfolio exposure to both Australian and Global Investment markets.

-1.png?width=352&name=Investment%20SnapShot%20Header%20-%20July%202025%20(1)-1.png)