-1.png)

Weekly recap

What happened in markets

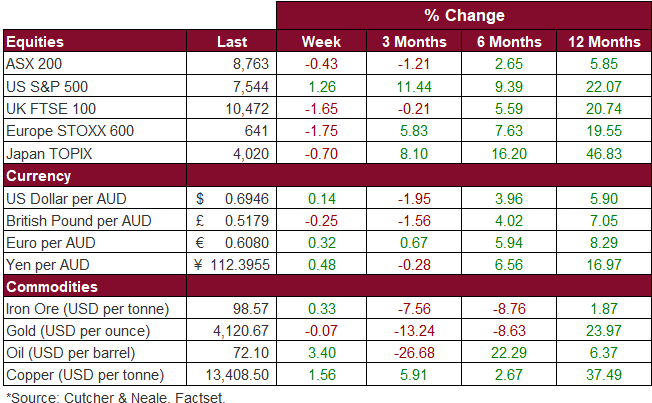

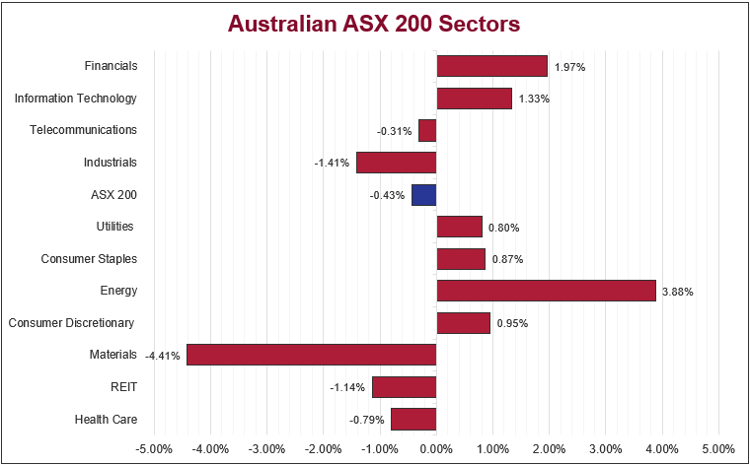

The Australian sharemarket declined last week, with the ASX200 down around 0.4%, as persistent geopolitical tensions and rising bond yields weighed on sentiment. The market traded weaker through most sessions, despite multiple intraday recoveries, reflecting cautious positioning amid uncertainty around US-Iran tensions and central bank outlooks. The Materials sector was a key laggard, down 4.4%, despite a late bounce back on Friday. Sector heavyweights BHP and Rio Tinto dropped 3.7% and 3.9% respectively. In contrast, the Energy sector jumped 3.9%, supported by higher oil prices, while Financials added 2.0%, as the major banks edged higher. The week concluded with a rebound on Friday, led by strength in mining and banks, though this was not enough to offset earlier loses.

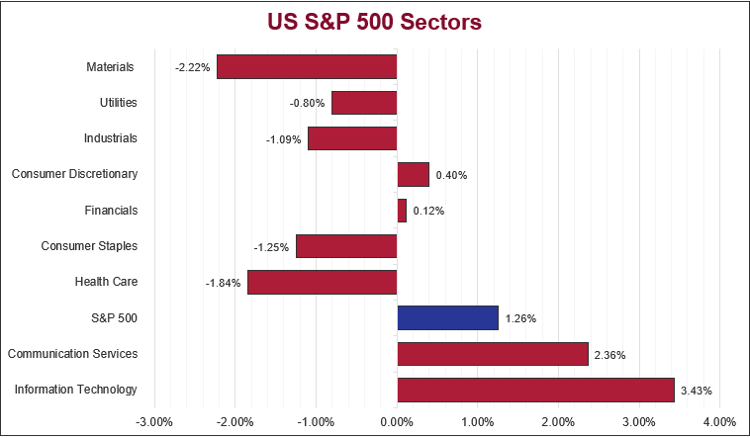

US sharemarkets were higher over the week, with the S&P 500 (1.3%) and Nasdaq (1.7%) both rising. Gains were driven largely by strength in large-cap technology stocks. NVIDIA, advanced 8.3%, on reports that China would allow limited purchases of its H200 chips, easing prior demand concerns. Additionally, Micron Technology announced plans of investing more than US$250 billion in America through to 2035, due to demand in memory chips, while Celestica (7.0%) also benefitted from the ongoing AI optimism. However, rising bond yields and oil prices weighed on broader market participation, limiting gains outside of mega-cap stocks. Geopolitical tensions in the Middle East added volatility, contributing to higher oil prices and risk uncertainty.

European sharemarkets fell over the week, with the STOXX Europe 600 down 1.8%, as rising yields and geopolitical tensions weighed on sentiment. Escalation in the Middle East pushed oil prices higher and reinforced expectations for further interest rate tightening, creating headwinds for equities. Political uncertainty in the UK and France added further pressure, alongside mixed economic data including weaker UK business confidence. Semiconductor stocks experienced some volatility, with SK Hynix declining 7.8% as investors took profits amid rising yields and a rotation away from momentum trades. The Materials sector was the worst performing, falling 5.1%, which saw London listed Rio Tinto (-4.5%) and Glencore (-0.6%) both drop.

Stock & sector movements

What caught our eye

The Subscription Nobody Budgeted For

For the past three years the AI story has largely been told through the spending plans of technology giants. New consumer surveys suggest it is now being told through household budgets as well.

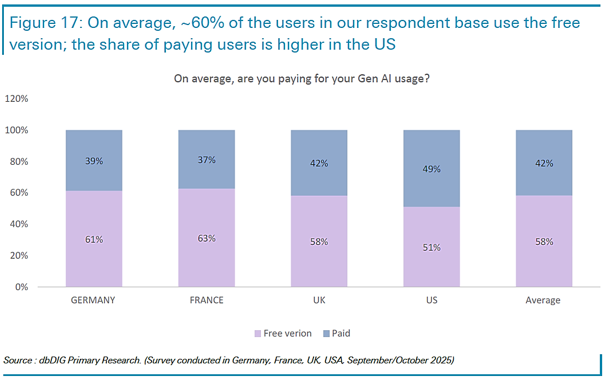

The revenue side of AI has begun to arrive, in the most ordinary way possible, as a line in the family subscription wallet. Deutsche Bank has tracked consumer subscription habits in Germany, the UK and the US since 2022. Its latest survey found the average respondent now spends about US$92 a month across nine categories such as video, music and news. For the first time, AI sits alongside them. Average spending on AI subscriptions is already around US$20 a month. That is a category that simply did not exist when the survey began. Half of US consumers now use AI at least weekly, and one in five online searches begins on an AI model rather than a browser.

About half the survey population has used ChatGPT in recent months, and roughly 42% of those using AI tools now pay for them, a share that rises to nearly half in the US. Most paying users spend under US$50 a month, often spread across several models. Many users ranked AI as their single most important subscription, with many saying they would cancel every streaming service they hold before giving it up. Habits like this are the foundation of durable subscription businesses, as investors in music and video streaming learned over the past decade.

The opportunity ahead is far larger than the revenue has booked so far. The share of US adults using generative AI has climbed from 7% to 41% in three years, faster than the internet, the smartphone or social media spread. Only 9% of US consumers currently pay for AI, against 75% for video streaming and 43% for music, so merely matching music streaming norms would expand the paid base roughly five times over.

UBS surveyed more than 3,000 people across the US, Europe and China and found that 80% now use an AI product, with ChatGPT alone reaching roughly 900 million weekly users. Yet 94% of those users pay nothing at all. That gap helps explain why advertising tiers have begun to appear, and the survey evidence suggests consumers will wear them. Only 22% said they would stop using the tools if ads were introduced, while another 15% said they would upgrade to a paid version to avoid them. Either response produces revenue.

This data is encouraging for those invested in AI beneficiaries. The pipes have been laid and the first revenue is now flowing through them, which is exactly what a maturing investment theme should look like. The Cutcher & Neale International Shares Model holds meaningful positions in Alphabet, Microsoft, Amazon and NVIDIA, four businesses on both sides of the AI transaction. Alphabet has grown Gemini to roughly 750 million monthly users, Microsoft’s Copilot reaches three in ten consumers surveyed and has close access to enterprises. Both collect the new subscription and advertising dollars directly. Amazon sits at the top of the video streaming wallet, while its cloud division sells the computing that AI services run on. NVIDIA designs the chips and software that run the AI models, while other holdings like SK Hynix and Applied Materials supply the memory and manufacturing equipment. Further upstream, holdings like Caterpillar and GE Vernova build and power the data centres needed for AI. Survey evidence like this underpins our confidence in those companies because it shows their enormous AI investment is being met by genuine recurring consumer revenue. And importantly, this is still only the consumer story. Enterprise adoption and the emerging wave of agentic AI are likely to add another layer of demand in the years ahead.

The week ahead

Locally, the focus will be on key sentiment indicators, including Westpac consumer confidence, NAB business confidence and inflation expectations, providing insight into the resilience of households and businesses.

Overseas, attention will centre on US economic data, particularly the June CPI release on Tuesday, alongside retail sales, producer prices and jobless claims later in the week. Investors will also closely watch the start of the US earnings season, with major banks reporting results and setting the tone for corporate earnings. In Europe, markets will look to CPI data for further direction on inflation trends and interest rate expectations.

Wade is the head of the Investment Services division at Cutcher & Neale and has over 15 years of industry experience in accounting and investment advisory roles.

Wade guides his division on the belief that investment portfolios should be built on transparency and flexibility. His expertise focuses on direct portfolio exposure to both Australian and Global Investment markets.

.png?width=352&name=Investment%20SnapShot%20Header%20-%20July%202025%20(1).png)