-1.png)

Weekly recap

What happened in markets

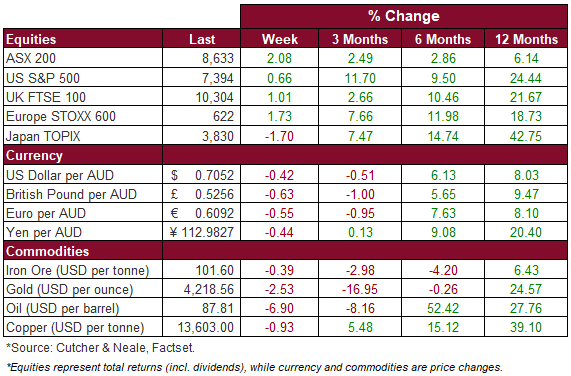

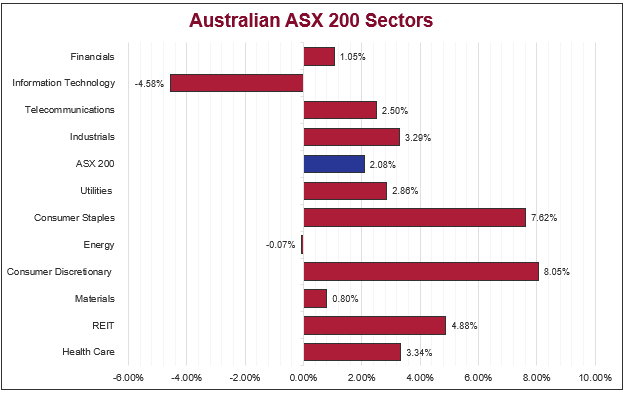

The Australian sharemarket rebounded over the week, with the ASX 200 rising 2.08%, recovering from the prior week’s softness and taking direction from stronger global markets. While the headline result was positive, investor sentiment remains cautious. Ongoing uncertainty around interest rates and the broader economic outlook continues to keep markets data‑dependent. The Consumer Discretionary (8.05%) and Consumer Staples (7.62%) sectors rocketed higher with major retail outlets posting strong returns, including Westfarmers (9.55%) and JB Hi-FI (7.16%) with a slight shift to value over growth at current prices. Further supported by the selloff in the Information Technology sector (-4.58%) over the week, with Energy (-0.07%) the only other sector to finish down.

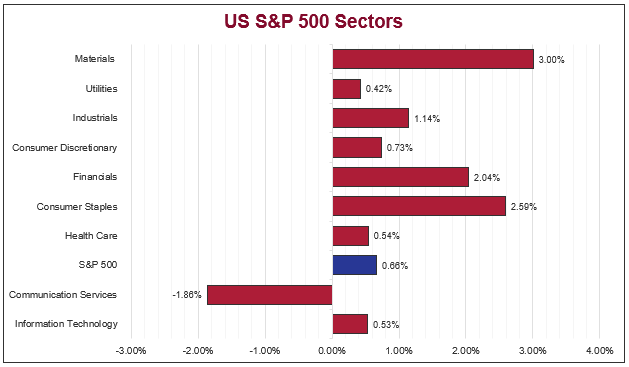

US sharemarkets edged higher over the week, the S&P 500 up 0.66%. Sentiment remains strong in AI-related names, propelled by the SpaceX IPO launch, which shattered market expectations and became the biggest IPO launch in history. The Materials Sector led the index advancing 3.00%, followed by the Consumer Staples (2.59%) and Financials (2.04%). The Technology (0.53%) sector was mixed, with strong returns in Intel Corporation (25.61%) and Applied Material (25.22%) however, there were sizeable downturns in Autodesk (-13.71%) and Adobe (-18.86%). The Communication Services (-1.86%) and Energy (-0.35%) Sectors were the only two to drag on the index. Overall, the index posted solid gains, driven by anticipation of a deal between the US and Iran, which was announced this morning by President Trump. The deal has opened the Strait of Hormuz ‘permanently and toll free’.

European sharemarkets ended the week strong, with returns of 1.73% on the STOXX Europe 600. All major sectors, apart from Energy (-1.40%) finished in the green. Despite the ECB shifting it’s interest rate policy stance and raising its policy rate 25 basis points to 2.4%, the Technology sector (2.78%) delivered strong gains, with ASML Holding rocketing 11.45% following commentary from Elon Musk at the company’s conference about chip manufacturing and future collaboration between his technology companies and the semiconductor manufacturer. Additionally, the Travel & Leisure (3.86%), Retail (2.89%) and Banks (2.84%) all posted strong returns, supported by energy prices easing and improved stability in credit conditions following the ECB’s rate increase.

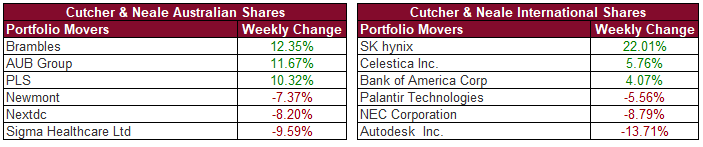

Stock & sector movements

What caught our eye

The Cutting Cycle Stalls on an Oil Shock

For most of 2025 inflation was falling, central banks were cutting rates, and markets could plan around both. That has now changed, and three central bank meetings this week and next show how quickly things can change.

The same problem links all three. The conflict in the Middle East and the disruption to shipping through the Strait of Hormuz have pushed fuel costs sharply higher. Those higher costs are now lifting prices more broadly. This is the awkward kind of inflation. It comes from supply rather than from economies running too hot, which means higher interest rates work against it only slowly and at a real cost to growth.

The European Central Bank moved first. Last Thursday it lifted its deposit rate by a quarter point to 2.25%, its first increase since 2023. The ECB has a simpler job than most of its peers because its mandate is price stability alone, with no requirement to weigh employment. With euro area inflation back at 3.2% in May and underlying measures still climbing, the decision was straightforward, even as the bank trimmed its growth forecasts for the next two years.

Closer to home, the RBA meets on Tuesday and is widely expected to leave the cash rate at 4.35% after three increases already this year. The real argument is about what comes next. Westpac thinks the same energy shock will force the board to raise again in August and September, now seeing headline inflation peaking near 4.7%. Commonwealth Bank reads the soft local data differently, pointing to a weak April jobs report as reason to hold and eventually cut next year. Both agree June is a pause, and that the wording of the statement will tell us more than the decision itself.

Then there is the US Federal Reserve, which meets on the 16th and 17th of June for the first time under Kevin Warsh. He arrives with a firm labour market, inflation at 4.2% in May and US President Donald Trump openly pushing for lower rates. Cutting rates while jobs are strong and prices are rising would be hard to defend, and markets know it. They now price roughly one increase over the next 6 to 12 months rather than any cut at all.

For investors, the practical point is that the rate cuts many expected in 2026 are no longer coming, at least not on the old timetable. We would not read that as cause for alarm. Much of this inflation comes from a single supply shock, and if the conflict settles and shipping through the strait returns to normal, the pressure should fade almost as quickly as it arrived.

That is why we are watching the Middle East at least as closely as the monthly inflation figures, because right now it is the conflict, not the data, that will decide where rates go from here.

The week ahead

In Australia, the main focus will be on the RBA interest rate decision this Tuesday, with market consensus being that the RBA will hold interest rates at 4.35%.

Overseas, attention will also shift to the Federal Reserve’s interest rate decision, with forecasts predicting rates to hold steady at 3.75%. In Europe, major data will be centered around inflation figures on Wednesday.

Wade is the head of the Investment Services division at Cutcher & Neale and has over 15 years of industry experience in accounting and investment advisory roles.

Wade guides his division on the belief that investment portfolios should be built on transparency and flexibility. His expertise focuses on direct portfolio exposure to both Australian and Global Investment markets.

.png?width=352&name=Investment%20SnapShot%20Header%20-%20July%202025%20(1).png)