Pre-Open Data

Key Data for the Week

Key economic data released this week:

- Thursday – AUS – Unemployment Rate fell to 6.8% in November, from 7.0% in October. 90,000 jobs were created in November and the participation rate rose to 66.1%.

- Thursday – UK – BoE Interest Rate Decision remained unchanged at 0.1% as expected.

- Friday – UK – Consumer Confidence

- Friday – UK – Retail Sales

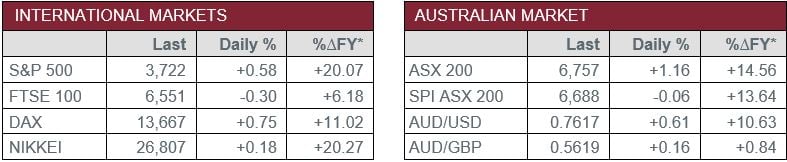

Australian Market

The Australian sharemarket rose 1.2% yesterday, boosted by better employment and budget reports. All sectors closed higher with Information Technology, Energy and Materials the strongest performers. Afterpay rose 5.0% to hit a new record high, while Zip Co added 1.1% after raising $120 million from institutional investors to fund global growth in the US & UK and to drive its Zip Business brand in Australia.

Mining heavyweights helped lift the Materials sector; BHP and Rio Tinto both added 1.8%, while Fortescue Metals rose 2.0%.

The Financials sector also posted strong gains, as the big four banks all rose between 0.6% and 1.3%.

Sydney’s coronavirus cluster prompted concerns about states possible reintroduction of border closures. Travel stocks Flight Centre and Webjet both fell 3.0%, while Helloworld Travel slipped 5.5%.

A2 Milk had its shares placed in a trading halt after it said it needed to revise its earnings guidance. Freedom Foods remains in a trading halt as the company announced it sold its cereals and snacks operations to Arnott's for $20 million as it focuses on dairy, nutritional and drink products.

The Australian futures market points to a relatively flat open today.

Overseas Markets

European sharemarkets were mostly higher on Thursday, as hopes of more stimulus in the United States and potential COVID-19 vaccine rollouts in Europe strengthened the case for a global economic recovery. The broad based STOXX Europe 600 added 0.3% and Germany’s DAX lifted 0.8% to close at its highest level since February, while the UK FTSE 100 slipped 0.3%.

US sharemarkets were also higher overnight. The Health Care sector was amongst the best performer as Johnson & Johnson and Illumina rose 2.6% and 2.3% respectively. Financial services companies also outperformed, led higher by PayPal, up 2.3%, while MasterCard added 1.5% and Visa rose 1.4%. Technology and Consumer stocks underperformed; Amazon slipped 0.2%, while Alphabet and Facebook fell 0.8% and 0.4% respectively.

By the close of trade, the Dow Jones gained 0.5%, the S&P 500 rose 0.6% and the NASDAQ added 0.8%.

CNIS Perspective

Don’t expect the US Federal Reserve to end its massive asset support program anytime soon. This was the clear message this week as the Federal Open Market Committee (FOMC) stated it would continue to buy at least US$120 billion of debt per month “until substantial further progress has been made toward the Committee’s maximum employment and price stability goals”, laying out a roadmap that could keep the ‘pump-priming’ strategy going for several years. This is contrary to previous messages from the FOMC which had alluded to support for “several months”.

This updated language on debt and its ‘outcomes-based’ approach mirrors the FOMC’s pledge to keep interest rates close to zero until the economy reaches full employment and inflation returns to its 2% target. Given current forecasts don’t see inflation moving to 2% until 2023, it is likely low interest rates will continue for several years.

Federal Reserve officials also elevated their outlook on the economy and now expect US GDP to be -2.4% versus -3.7% previously and to rebound 4.2% in 2021 versus 4.0% previously. US unemployment is projected to hold steady at 6.7% by year’s end, down from the Fed’s 7.6% previous forecast, with the jobless rate recovering faster than expected.

Despite this economic recovery and a potential vaccine on the horizon, it is becoming clearer the US central bank intends to keep financial conditions extremely accommodative for some time to come.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.