Pre-Open Data

Key Data for the Week

- Monday – CHINA – Gross Domestic Product

- Monday – UK – Rightmove House Prices Index

- Monday – US – Industrial Production

- Tuesday – US – Building Permits

- Wednesday – EUR – Consumer Price Index

- Wednesday – UK – Consumer Price Index

- Thursday – AUS – NAB Business Confidence

- Thursday – US – Existing Home Sales

- Friday – EUR – Markit Manufacturing PMI

- Friday – UK – Retail Sales

- Friday – US – Markit Manufacturing PMI

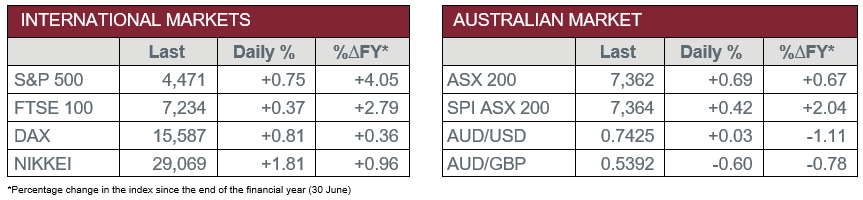

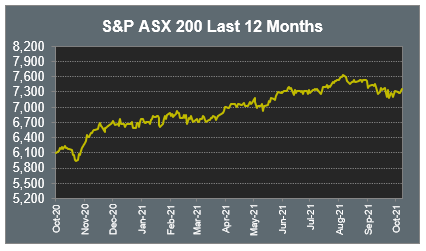

Australian Market

The Australian sharemarket advanced 0.7% on Friday. All sectors except Utilities enjoyed gains, with the Information Technology the strongest performer, up 1.4%.

Travel stocks rallied following the announcement that NSW will allow quarantine-free international travel from 1 November 2021. Helloworld Travel climbed 6.3% and Regional Express Holdings jumped 6.2%, while Webjet added 4.1% and Qantas rose 2.0% after the airline announced international flights will resume two weeks earlier than previously stated.

Mining heavyweights BHP and Fortescue Metals lifted 2.8% and 2.0% respectively on stronger commodity prices. However, Rio Tinto gave up 0.9% after the miner’s quarterly update revealed a decline in the production of some of the major commodities, lowering forecasts for iron ore exports.

The Australian futures market points to a 0.42% rise today, driven by stronger overseas markets.

Overseas Markets

European sharemarkets were higher on Friday. Banks were the key outperformer following stronger-than-expected quarterly results from US lenders; Lloyds Bank and Barclays Bank added 1.4% and 1.8% respectively, while Credit Suisse rose 1.9% and Deutsche Bank lifted 3.2%. Energy stocks also improved; Royal Dutch Shell added 1.6% and BP closed up 1.7%.

By the close of trade, the UK FTSE 100 lifted 0.4%, while the STOXX Europe 600 and German DAX rose 0.7% and 0.8% respectively.

US sharemarkets also improved on Friday. The Consumer Discretionary sector led the gains; Amazon jumped 3.3% and Shopify rose 1.3%. Financial services stocks also advanced; PagSeguro Digital rallied 6.1% and MasterCard lifted 3.3%, while BlackRock added 1.7% and PayPal gained 0.7%. The Information Technology sector rose 0.8%; Apple lifted 0.8%, while NVIDIA and Microsoft both closed up 0.5%.

By the close of trade, the NASDAQ added 0.5% and the S&P 500 gained 0.8%, while the Dow Jones closed 1.1% higher.

Over the week, the Dow Jones lifted 1.6%, the S&P 500 rose 1.8% and the NASDAQ jumped 2.2%.

CNIS Perspective

Bitcoin broke through US$60,000 over the weekend on hopes that the US Securities and Exchange Commission won’t object to the first US-listed exchange traded funds (ETFs) in cryptocurrency. This is anticipated to open the floodgates to a stream of products and new investors who prefer traditional ways of accessing investments via a stock exchange instead of the many cryptocurrency exchanges.

Further access and regulatory oversight will increase adoption and provide validation, making conservative investors feel more comfortable in this burgeoning asset class, with pension funds now seeking to add exposure. Australia’s fifth largest pension fund, Queensland Investment Corporation (QIC), which manages $92 billion, has announced last week it will be considering investing into the mercurial and polarising world of digital assets.

For many investors the real interest lies not with the coins such as Bitcoin, but with the blockchain technology underlying cryptocurrencies. This is often talked about as Web 3.0, where internet and application services are powered by distributed ledger technology. Regardless of the investment approach taken as the industry matures from a Wild West market, further entry of large banks and other financial institutions highlight the perceived opportunity.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.