.png)

|

|

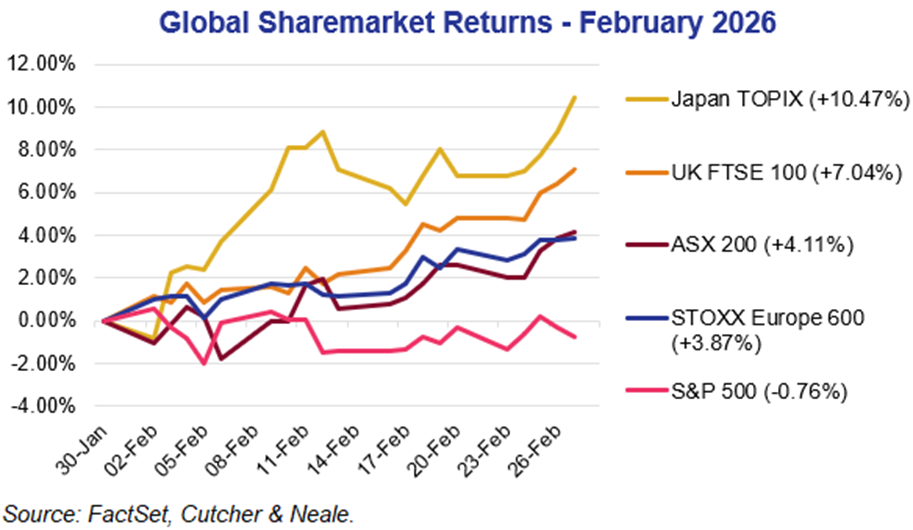

Quick TakeGlobal markets were mixed but constructive in February: US equities softened, while Europe and Australia pushed higher as investors continued to rotate beneath the surface. The S&P 500 fell 0.76% and the Nasdaq declined 3.33%, while the Russell 2000 rose 0.80%. In contrast, the STOXX Europe 600 gained 3.87% to fresh record highs and the ASX 200 advanced 4.11% to sit just below its 52-week high. Bond yields generally eased and gold rallied strongly. In the US, the theme was rotation rather than a broad risk off move: Large technology stocks lagged amid ongoing debate about the pace, costs, and returns of artificial intelligence investment, while equal weighted measures of the market outperformed. Economic conditions remained supportive, with strong payrolls and steady activity indicators. The Federal Reserve held rates steady, while markets continued to expect two 0.25% rate cuts later in 2026. Trade and geopolitics also returned to the foreground, including a new 10% global tariff and renewed Middle East conflict that added to oil price volatility. In Europe and Australia, improving momentum met active central banks: Europe’s rally persisted as macro indicators stabilised, the ECB kept rates unchanged, and the Bank of England held its policy rate at 3.75%, while markets looked for easing ahead. In Australia, the RBA lifted the cash rate 0.25% to 3.85% in response to persistent inflation, while the ASX 200 rose 4.11% and the Australian Dollar strengthened 1.7% to around US$0.7127. Overall, resilient growth and earnings helped sustain confidence despite ongoing uncertainty around inflation, rates, and global trade policy. |

|

Snapshot

Global equity markets delivered a mixed but generally constructive performance in February, as investors rotated beneath the surface of headline index moves. In the US, the S&P 500 declined 0.76% and the Nasdaq fell 3.33%, recording its weakest month since March 2025. In contrast, the Russell 2000 gained 0.80%, highlighting a continued shift toward smaller companies and more economically sensitive exposures. European markets extended their strong run, with the STOXX Europe 600 rising 3.87% to fresh record highs. In Australia, the ASX 200 advanced 4.11%, finishing just below its 52-week high. Bond yields generally eased across developed markets and gold prices rallied strongly.

Global equity markets delivered a mixed but generally constructive performance in February, as investors rotated beneath the surface of headline index moves. In the US, the S&P 500 declined 0.76% and the Nasdaq fell 3.33%, recording its weakest month since March 2025. In contrast, the Russell 2000 gained 0.80%, highlighting a continued shift toward smaller companies and more economically sensitive exposures. European markets extended their strong run, with the STOXX Europe 600 rising 3.87% to fresh record highs. In Australia, the ASX 200 advanced 4.11%, finishing just below its 52-week high. Bond yields generally eased across developed markets and gold prices rallied strongly.

In the US, February was characterised less by broad risk aversion and more by rotation. Ongoing debate around the pace and implications of artificial intelligence investment weighed on large technology companies, even as the broader market showed resilience. Beneath the modest decline in the S&P 500, equal weighted measures of the market outperformed, suggesting capital was rotating rather than exiting equities altogether. Economic data remained supportive, with January payrolls surprising to the upside and activity indicators holding firm. The Federal Reserve left rates unchanged and reiterated a data dependent approach, while markets continued to price two 0.25% rate cuts later in 2026, with the first expected around mid-year. Trade policy also returned to focus after the US Supreme Court ruled against the use of certain emergency tariff powers, prompting the administration to introduce a new 10% global tariff. Geopolitical conflict in the Middle East contributed to volatility in oil prices during February and into March.

European equities extended their momentum, with the STOXX Europe 600 rising 3.87% and marking its eighth consecutive monthly gain. Investor confidence was underpinned by improving macroeconomic indicators across the Euro area and the United Kingdom, alongside steady central bank policy settings. The European Central Bank left rates unchanged, noting inflation was close to target at 1.7%, while core measures remained around 2.2%. In the United Kingdom, the Bank of England held its policy rate at 3.75%, though markets increasingly expect easing in coming months as growth remains subdued and inflation moderates. While headlines around artificial intelligence disruption created volatility in some segments of the market, investors largely viewed any pullbacks as opportunities against a backdrop of stabilising growth and attractive relative valuations. Geopolitical risks, including renewed US tariff measures and ongoing tensions involving Russia and Iran, were monitored but did not materially derail the region’s rally.

European equities extended their momentum, with the STOXX Europe 600 rising 3.87% and marking its eighth consecutive monthly gain. Investor confidence was underpinned by improving macroeconomic indicators across the Euro area and the United Kingdom, alongside steady central bank policy settings. The European Central Bank left rates unchanged, noting inflation was close to target at 1.7%, while core measures remained around 2.2%. In the United Kingdom, the Bank of England held its policy rate at 3.75%, though markets increasingly expect easing in coming months as growth remains subdued and inflation moderates. While headlines around artificial intelligence disruption created volatility in some segments of the market, investors largely viewed any pullbacks as opportunities against a backdrop of stabilising growth and attractive relative valuations. Geopolitical risks, including renewed US tariff measures and ongoing tensions involving Russia and Iran, were monitored but did not materially derail the region’s rally.

In Australia, the ASX 200 rose 4.11% in February, supported by strength in commodity prices and the financial sector, even as parts of the market exposed to technology themes remained under pressure. The Reserve Bank of Australia increased the cash rate by 0.25% to 3.85%, citing persistent inflationary pressures and a tight labour market. January inflation data surprised to the upside, with non-tradeables like rent, wages, and clothing rising by 4.9% and electricity prices contributing to elevated headline readings. Employment conditions remained firm, reinforcing the central bank’s assessment that demand continues to run ahead of supply. Bond yields declined modestly over the month, with the 10-Year Government Bond yield easing to 4.63% from 4.80%. The Australian Dollar strengthened 1.7% to finish near US$0.7127.

Overall, February highlighted a market environment defined by rotation rather than retreat. While technology heavy indices in the US came under pressure, broader participation improved, Europe continued to benefit from cyclical recovery and capital inflows, and Australian equities reached new highs despite tighter monetary policy. Investors remain focused on the path of inflation, interest rates and global trade policy, but resilient economic conditions and solid corporate earnings have so far helped sustain confidence as 2026 progresses.

Overall, February highlighted a market environment defined by rotation rather than retreat. While technology heavy indices in the US came under pressure, broader participation improved, Europe continued to benefit from cyclical recovery and capital inflows, and Australian equities reached new highs despite tighter monetary policy. Investors remain focused on the path of inflation, interest rates and global trade policy, but resilient economic conditions and solid corporate earnings have so far helped sustain confidence as 2026 progresses.

Key Stocks

Ryan joined Cutcher & Neale as a Portfolio Manager in January 2023, bringing nearly 20 years of financial markets experience to the firm. Specialising in fundamental equity analysis and multi-asset strategies, Ryan holds the Chartered Financial Analyst (CFA) designation. He is responsible for the risk and return outcomes of the firm’s Managed Discretionary Account (MDA) portfolios on the Mason Stevens platform.

.png?width=352&name=Investment%20SnapShot%20Header%20-%202026%20(3).png)