Pre-Open Data

Key Data for the Week

- Friday – UK – Nationwide House Prices

- Friday – AUS – Producer Price Index

- Friday – EUR – Consumer Price Index

Australian Market

The Australian sharemarket rebounded 1.3% on Thursday, after all sectors closed ahead except Telecommunications (-0.1%). The market was pushed higher by the Materials (3.5%) sector, with BHP (4.4%), Rio Tinto (3.5%) and Mineral Resources (4.8%) being key contributors.

In company news, Fortescue Metals Group surged 8.1%, after it reported iron ore shipments in the third quarter were up 10% year on year and upgraded its FY2022 guidance. Furthermore, Pilbara Minerals closed up 3.5%, despite its report that production had eased, the tight labour market had led to staff shortages and shipments fell ~25% due to port delays. Meanwhile, Coles was 0.6% higher, after it posted a 3.6% uplift in quarterly sales.

AMP was the best performer in yesterday’s session, up 13.2%, after news it agreed to sell Collimate Capital, its international infrastructure equity business, to DigitalBridge Group Inc. The deal will see AMP receive $699 million.

The Financials sector performed modestly on Thursday, as most major banks closed in the green. Westpac and ANZ both rose between 0.6-0.7%, while Commonwealth Bank inched 0.2% higher and NAB was relatively flat.

The Australian futures market points to an increase of 0.68% today.

Overseas Markets

European sharemarkets pushed higher on Thursday, as positive earnings results encouraged investors and eased concerns about slowing economic growth. A key reporter in the session included Volvo Cars (8.0%), after its profit beat analyst forecasts as demand for its products remained strong. Meanwhile, major oil company TotalEnergies (3.7%) reported positively, unsurprising given elevated global oil prices in recent months, and announced plans to buy back an additional US$2 billion of its own shares by the end of June. By the close of trade, the STOXX Europe 600 lifted 0.6%, the UK FTSE 100 rose 1.1% and the German DAX advanced 1.4%.

US sharemarkets advanced on Thursday, after all sectors closed in the green, led by Information Technology (4.0%). Technology mega caps were important contributors in the session, as Microsoft (2.3%), Apple (4.5%), Alphabet (3.8%) and Netflix (5.8%) posted solid gains. However, Meta Platforms was the star performer, up 17.6%, after it reported revenue was 6.6% higher and daily users rose above expectations to 1.96 billion. These results were important as the stock had fallen almost 50% this year, as investors were increasingly concerned Facebook had lost steam. Other notable movers included ecommerce companies Visa (3.1%) and Amazon (4.7%). By the close of trade, the Dow Jones (1.9%), S&P 500 (2.5%) and NASDAQ (3.1%) all climbed higher.

CNIS Perspective

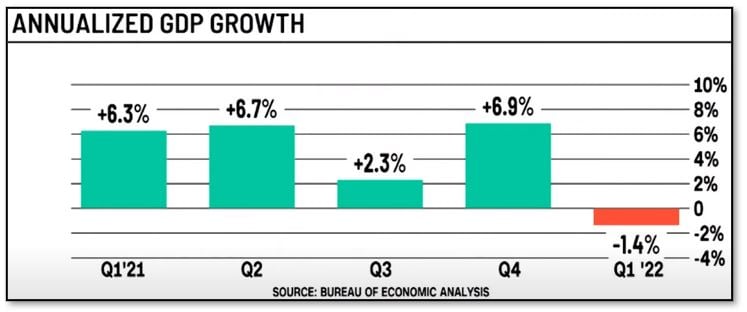

The US economy’s latest scorecard, GDP growth, the broadest measure of economic activity, was released overnight and showed a decline at an annualised rate of 1.4% between January and March, an abrupt reversal of the prior year's strong growth.

It was a marked slowdown from the 6.9% annualised pace of growth recorded in the December quarter of 2021 and the worst performance since the pandemic recession in the June quarter of 2020.

A number of factors contributed to the contraction, including rising Omicron infections, which hampered business activity, the Russian invasion of Ukraine, which increased energy costs and a growing trade deficit. What is interesting to note though is that consumer spending, which accounts for two-thirds of GDP, held up fairly well for the quarter, rising 2.7%, which reflects higher inflation feeding through to higher prices.

The GDP decline likely won’t change the immediate outlook for the Federal Reserve's monetary policy, with futures markets fully pricing a 0.50% increase next week, but all eyes will be on the June quarter’s GDP result to see if the US record a second straight quarter of negative GDP growth, a technical recession.

Should you wish to discuss this or any other investment related matter, please contact your Wealth Management Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.