Pre-Open Data

Key Data for the Week

- Thursday – AUS – Consumer Inflation Expectations increased to 4.4% in June, up from 3.5% in May.

- Thursday – EUR – ECB Monetary Policy – The ECB left interest rates unchanged at 0%.

- Friday – UK – Industrial Production

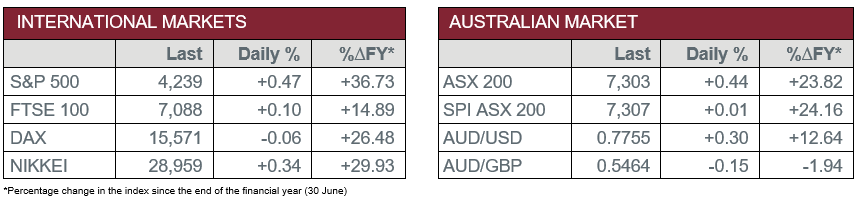

Australian Market

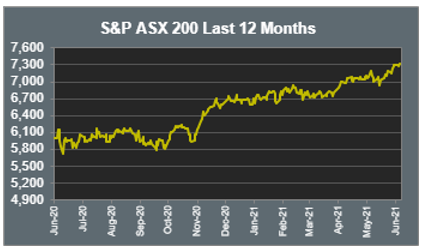

The Australian sharemarket lifted 0.4% on Thursday to reach a new record high. All sectors except Energy and Materials finished stronger, with REITs the top performer, up 2.4%. GPT Group rallied 3.8% and Stockland gained 3.2%, while Aventus Group and Goodman Group added 3.0% and 2.3% respectively.

The Information Technology sector was boosted by a 16.8% gain in financial services software company Iress. The gains followed a report by The Australian Financial Review that suggested investment bank Barrenjoey may purchase a stake in the company, however, Iress later released a statement confirming it had not received a direct approach. Buy-now-pay-later providers advanced; Afterpay and Sezzle both lifted 1.0%, while Zip Co added 0.7%.

The Consumer Staples sector was mixed; Coles lost 0.4% and Bega Cheese slipped 0.5%, while Woolworths closed up 0.8% after the ACCC allowed the supermarket giant to acquire 65% ownership of distributor PFD Food Services.

The Energy sector eased 1.1%, while the Materials sector finished the session flat; Oil Search shed 3.3%, while Woodside Petroleum and Beach Energy both fell 1.5%. Mining heavyweights were mixed; Fortescue Metals added 0.8% and Rio Tinto gained 0.1%, while BHP gave up 0.8%.

The Australian futures market points to a 0.01% rise today.

Overseas Markets

European sharemarkets were mixed overnight as the European Central Bank raised its recovery outlook and left interest rates unchanged. Automaker stocks weakened for the third consecutive day; BMW fell 1.9% and Volkswagen slipped 0.4%, while Porsche eased 0.3%. British telecommunications company BT Group climbed 6.6% after Altice Group announced it had taken a 12.1% stake in the company. By the close of trade, the UK FTSE 100 added 0.1% and the German DAX slipped 0.1%, while the broad based STOXX Europe 600 finished the session flat.

US sharemarkets advanced on Thursday despite the release of higher than expected inflation data, with the Consumer Price Index up 0.6% in for the month of May, exceeding consensus estimates of 0.4%. However, investors remained optimistic, as the release of economic data overnight supported the US Federal Reserves’ view that the current spike in inflation will be temporary. The Information Technology sector was a top performer; Spotify rallied 4.0% and Fortinet gained 1.5%, while Microsoft and Alphabet rose 1.4% and 1.2% respectively. Financial services stocks also enjoyed gains; PayPal added 2.2% and PagSeguro Digital lifted 1.6%, while Visa rose 0.7%. By the close of trade, the NASDAQ closed up 0.8% and the S&P 500 added 0.5%, while the Dow Jones lifted 0.1%.

CNIS Perspective

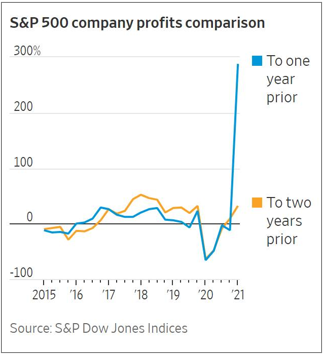

Like many aspects of the COVID-19 financial collapse and subsequent economic rebound, comparisons between this year’s and last year’s data looks like typos. Earnings Per Share for companies that make up the S&P 500 were up 225% in the first quarter this year from the corresponding period last year. According to S&P Global, this was in part due to the big hit taken during the January through March period of 2020.

The US Consumer Price Index was up 5.0% in May from a year earlier (announced overnight), more than double the Federal Reserve’s inflation target of 2%. However, a year ago COVID-19 was causing havoc for the economy and corporate profits. Demand for services like hotels, air flights and car rentals collapsed. The 5.0% comparison could provide an exaggerated snapshot of price pressures because it is from a deflated base in May 2020.

The Fed is now struggling with this challenge as it relates to inflation. Clearly prices are rising for both goods and services throughout the economy, however, statistics are misleading without the context. Quite possibly these base effects will fade later in 2021 as comparisons with 2020 become less dramatic.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.