Pre-Open Data

Key Data for the Week

- Wednesday – AUS – Westpac Lending Index fell to 0.5% in August, from 1.4%.

- Thursday – US – Markit Manufacturing PMI

- Thursday – UK – BoE Interest Rate Decision

- Thursday – US – Existing Home Sales

Australian Market

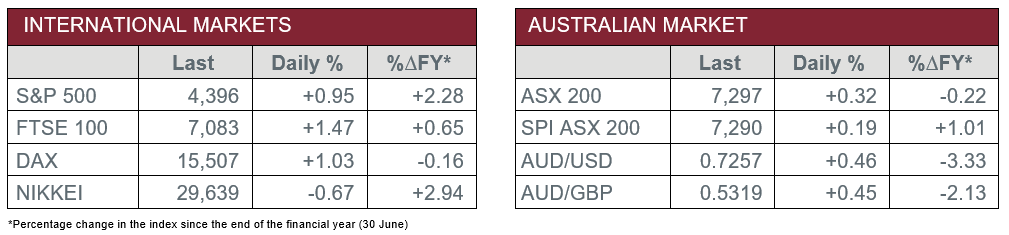

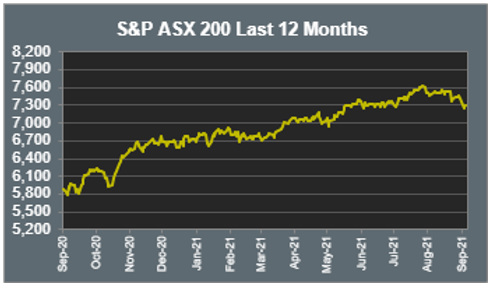

The Australian sharemarket slipped in the early stages of trading yesterday, although recovered to finish 0.3% higher. The recovery was due to news that Evergrande has committed to paying its bond interest due this week.

Having been heavily weakened earlier in the week as a result of the Evergrande issue, the Materials sector bounced 2.0% on Wednesday. The mining giants enjoyed gains; Fortescue Metals added 4.2%, Rio Tinto lifted 2.7% and BHP was up 2.4%. Goldminers also rose as Northern Star Resources and Evolution Mining gained 0.3% and 1.6% respectively.

The Energy sector was lifted by the major oil providers to close the day 2.3% higher. Woodside Petroleum added 2.4%, while Santos and Beach Energy rose 1.9% and 5.1% respectively.

Despite general market optimism, the Financials sector lost ground as concerns remain over the potential fallout if Evergrande is unable to repay its debt. ANZ shed 0.2%, while Commonwealth Bank and NAB both dropped 0.7%. Westpac closed the session 1.1% lower.

The Australian futures point to a 0.19% gain today, driven by stronger overseas markets.

Overseas Markets

European sharemarkets lifted overnight, relieved by the news Evergrande is able to meet its payment due this week. The Travel & Leisure sector enjoyed gains; Ryanair Holdings added 0.3%, easyJet lifted 0.7% and Lufthansa gained 3.7%. The Financial sector also lifted as Deutsche Bank and ING Groep added 3.9% and 2.7% respectively. By the close of trade, the German DAX and the STOXX Europe 600 both lifted 1.0%, while the UK FTSE 100 gained 1.5%.

US sharemarkets ended higher on Wednesday, as investor optimism was improved by the evolving Evergrande situation. Apple, Amazon and Alphabet all added more than 0.9%, recouping some of the losses suffered during the week. By the close of trade, the Dow Jones, S&P 500 and NASDAQ all added 1.0%.

CNIS Perspective

A build-up of economic excess in any economy is cause for concern, and the excesses of China’s Real Estate sector is reaching that point, similar to the excesses in the US in 2008 ahead of the banking crisis.

China’s Real Estate and Banking sectors have become the key bubble assets of their economy in recent decades and the Evergrande is a key example of that.

Evergrande is the most indebted property developer in the world and its liabilities equate to around 3% of China’s GDP. The outcome of its current financial predicament is therefore important!

The big question is: How big will the fallout be, and will it be orderly and contained with sufficient response from policy makers?

Given the size of Evergrande within the Real Estate sector and the importance of real estate to the Chinese economy, it appears likely the authorities will ringfence Evergrande.

The Chinese Government has delivered larger bail outs in the past, including the four largest banks in 1998, at a relatively higher cost than Evergrande.

History would suggest the Evergrande situation should therefore also qualify for policy support.

While a major crisis in China may be averted, it does indicate that fading momentum is underway in China’s economy.

Whether the economic excess that’s built-up during China’s extraordinary growth over recent decades reaches breaking point, will be closely watched.

Should you wish to discuss this or any other investment related matter, please contact your Investment Services Team on (02) 4928 8500.

Disclaimer

The material contained in this publication is the nature of the general comment only, and neither purports, nor is intended to be advice on any particular matter. Persons should not act nor rely upon any information contained in or implied by this publication without seeking appropriate professional advice which relates specifically to his/her particular circumstances. Cutcher & Neale Investment Services Pty Limited expressly disclaim all and any liability to any person, whether a client of Cutcher & Neale Investment Services Pty Limited or not, who acts or fails to act as a consequence of reliance upon the whole or any part of this publication.

Cutcher & Neale Investment Services Pty Limited ABN 38 107 536 783 is a Corporate Authorised Representative of Cutcher & Neale Financial Services Pty Ltd ABN 22 160 682 879 AFSL 433814.